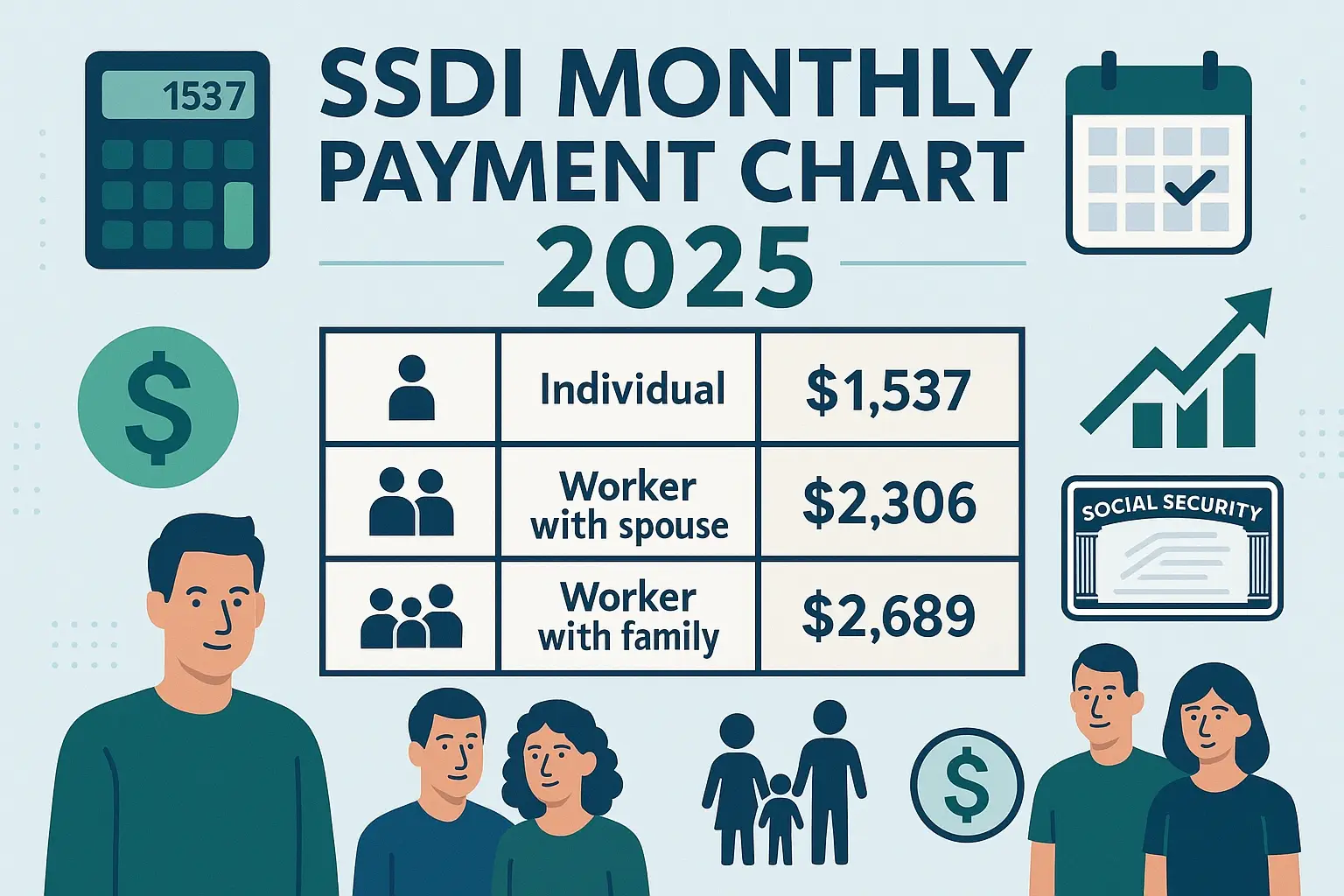

SSDI gives disabled workers a reliable monthly payment when health conditions prevent them from earning wages. This program is a safety net to replace lost income during long-term disability or blindness. It provides financial protection and helps maintain stability for individuals facing unexpected medical challenges. Without SSDI, many families would struggle with bills, housing, and access to necessary medical treatment.

Freelancers and contractors may still qualify for SSDI if they consistently pay Social Security taxes on reported earnings. These contributions demonstrate work history, which the Social Security Administration reviews carefully during the disability application process. A strong tax compliance record helps self-employed workers establish eligibility for future benefits. Without proper contributions, self-employed individuals risk losing coverage despite facing genuine disabling conditions.

SSDI safeguards taxpayers and small businesses against the devastating impact of total income loss. The Social Security Administration applies strict rules, requiring precise documentation and timely claims filing. Mistakes during the application may cause delays, denials, or significant financial hardship for applicants. By understanding these requirements, individuals and businesses protect themselves from sudden financial instability caused by disability.

Understanding SSDI for Self-Employed

Social Security Disability Insurance SSDI provides disability benefits when disability or blindness prevents a person’s ability to work in the United States. Self-employed workers and independent contractors qualify by paying self-employment tax and reporting net income after normal business expenses. The Social Security Administration applies a work test and examines whether work activity-based earnings reach the substantial gainful activity level. Monthly benefits help disabled workers and family members replace income lost after disability began.

Self-employed individuals must pay Social Security taxes and keep accurate gross income, net earnings, and countable income records. Excessive deductions for impairment-related work expenses or unpaid help may affect the countable income test used by the SSA. Approved SSDI benefits require accurate reporting of business expenses and honest disclosure of substantial income from self-employment activity. Without compliance, disabled workers risk losing disability insurance benefits, supplemental security income, and eventual retirement benefits under the Social Security Act.

Types of SSDI Considerations for the Self-Employed

Understanding the rules of Social Security Disability Insurance (SSDI) for self-employed individuals in the United States requires careful attention to income, taxes, and eligibility standards.

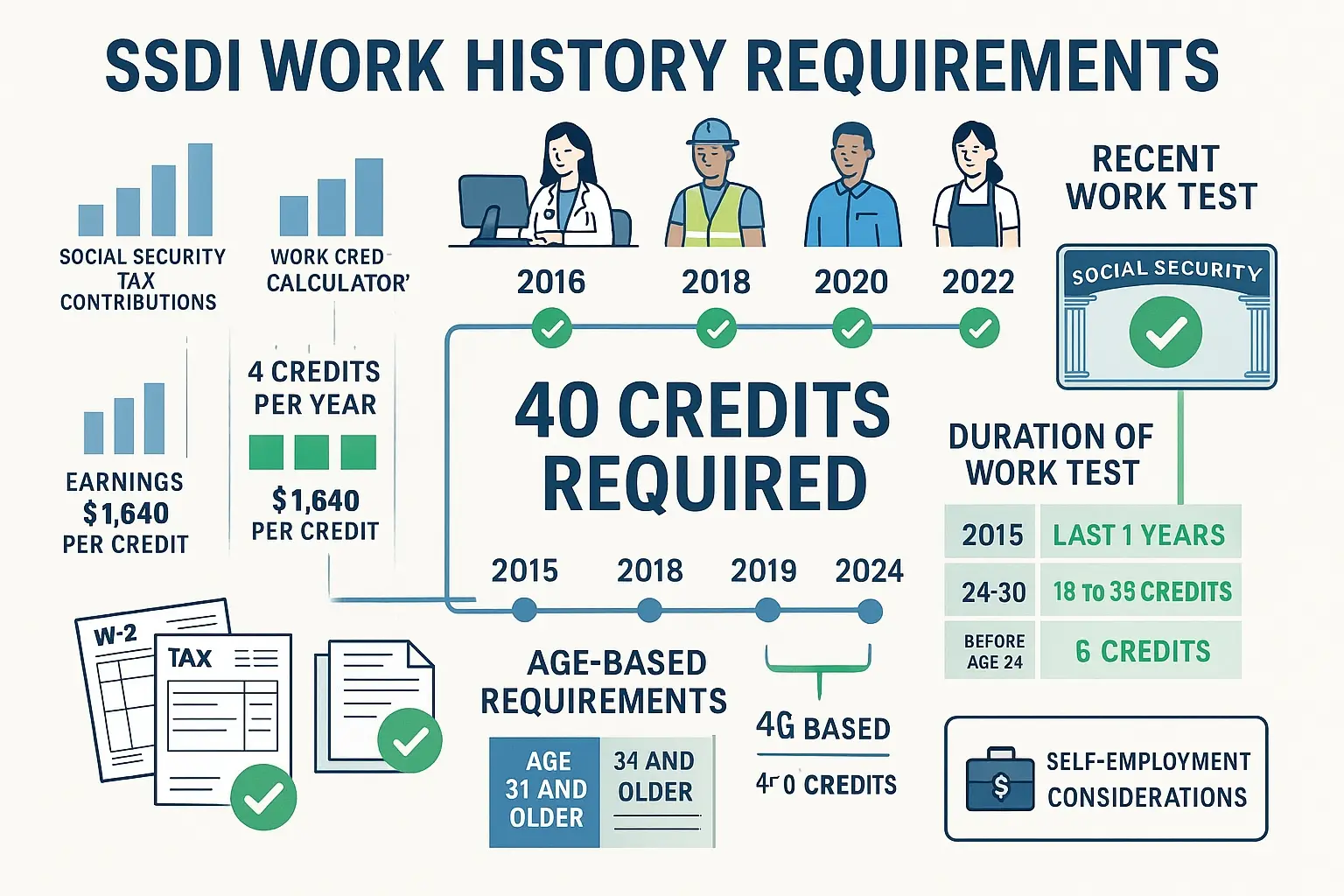

- Work Credits: You must earn work credits by paying self-employment tax and reporting net earnings under the Social Security Act. Each credit helps determine if you qualify for disability benefits through social security disability insurance. A younger disabled worker may need fewer credits, but proof of consistent contributions is always required. Work history remains a crucial factor for approval of monthly benefits.

- Substantial Gainful Activity: The Social Security Administration evaluates your ability to work by comparing earnings against the substantial gainful activity level. For disability or blindness, SSA sets higher income thresholds to determine if work activity is considered substantial. Income from self-employment or significant services may still disqualify you despite reduced hours. A work test helps decide if earnings are considered substantial under disability insurance benefits.

- Countable Income Test: SSA uses the countable income test to analyze gross income, net income, and normal business expenses. Self-employed workers must deduct impairment-related work expenses and report accurate self-employment income. Excessive deductions or unreported earnings may affect eligibility for social security disability benefits or supplemental security income. The countable income test ensures that only eligible self-employed individuals continue receiving SSDI benefits.

- Family Members: Family members like spouses or children may also qualify for benefits based on your disability insurance benefits record. Approved dependents may receive additional monthly benefits that supplement household security income. This support helps cover costs when a disabled worker can no longer maintain a substantial income. The SSA protects family members under the social security disability benefits rules.

Self-employed individuals must carefully manage their taxes, income, and records to remain eligible for SSDI benefits and protect their families.

Why Addressing SSDI for Self-Employed Matters

Social Security Disability Insurance provides disability insurance benefits that protect income when you can no longer manage your own business. The Social Security Administration ensures eligibility by reviewing your work history, tax records, and proof of disability or blindness. Once approved, monthly benefits grant access to Medicare and supplemental programs under the Social Security Act. These protections give financial stability to self-employed individuals who face limited alternatives in the United States.

SSDI benefits extend beyond the disabled worker by protecting family members who may also qualify under the approved disability insurance benefits record. Accurate reporting of self-employment income prevents complications with the IRS and Social Security Administration over unpaid self-employment tax. Sole proprietors, contractors, and independent workers must treat SSDI as essential, not optional, for long-term financial and medical security. By securing SSDI, you safeguard income, healthcare access, and dependents who rely on your work history and contributions.

Our Simple 4-Step Process

Filing for Social Security Disability Insurance SSDI as a self-employed worker can feel overwhelming, but a structured process simplifies everything.

- Case Assessment: We review your self-employment records, confirm social security taxes paid, and assess whether you meet SSA disability requirements. This step identifies strengths and weaknesses in your claim. A careful review ensures that disability insurance benefits align with your work history and reported income. Early evaluation prevents unnecessary delays in your disability benefits application.

- Eligibility and Needs Analysis: We confirm your disability or blindness status, verify earned work credits, and check your Social Security online account activity. This ensures compliance with the Social Security Act and eligibility for monthly benefits. We also examine the trial work period history to confirm substantial gainful activity. Proper analysis strengthens your case and prevents overlooked requirements.

- Document Preparation and Filing: We organize business expenses, medical records, and tax forms required for SSDI benefits. Every detail is documented, including impairment-related work expenses and countable income. Filing accuracy ensures your disability insurance benefits application meets strict SSA deadlines. Proper preparation improves your chances of approval on the first submission.

- Ongoing Support and Updates: We track SSA notices, explain decisions, and help appeal denials when necessary. We guide you through the countable income test if you return to self-employment. Ongoing support ensures you remain eligible for SSDI benefits while protecting your financial security. Regular updates give you confidence throughout your disability journey.

Our four-step process ensures your application for Social Security Disability benefits is accurate, complete, and fully compliant with SSA rules.