SSDI vs SSI: Why Understanding the Difference Matters

Many people know that the Social Security Administration (SSA) provides disability benefits, but confusion often arises when comparing Social Security Disability Insurance (SSDI) and Supplemental Security Income (SSI). At first glance, both programs seem similar—they both provide monthly benefits to people with disabilities. However, the rules, eligibility requirements, and payment amounts are unique.

The Key Differences Between SSDI and SSI

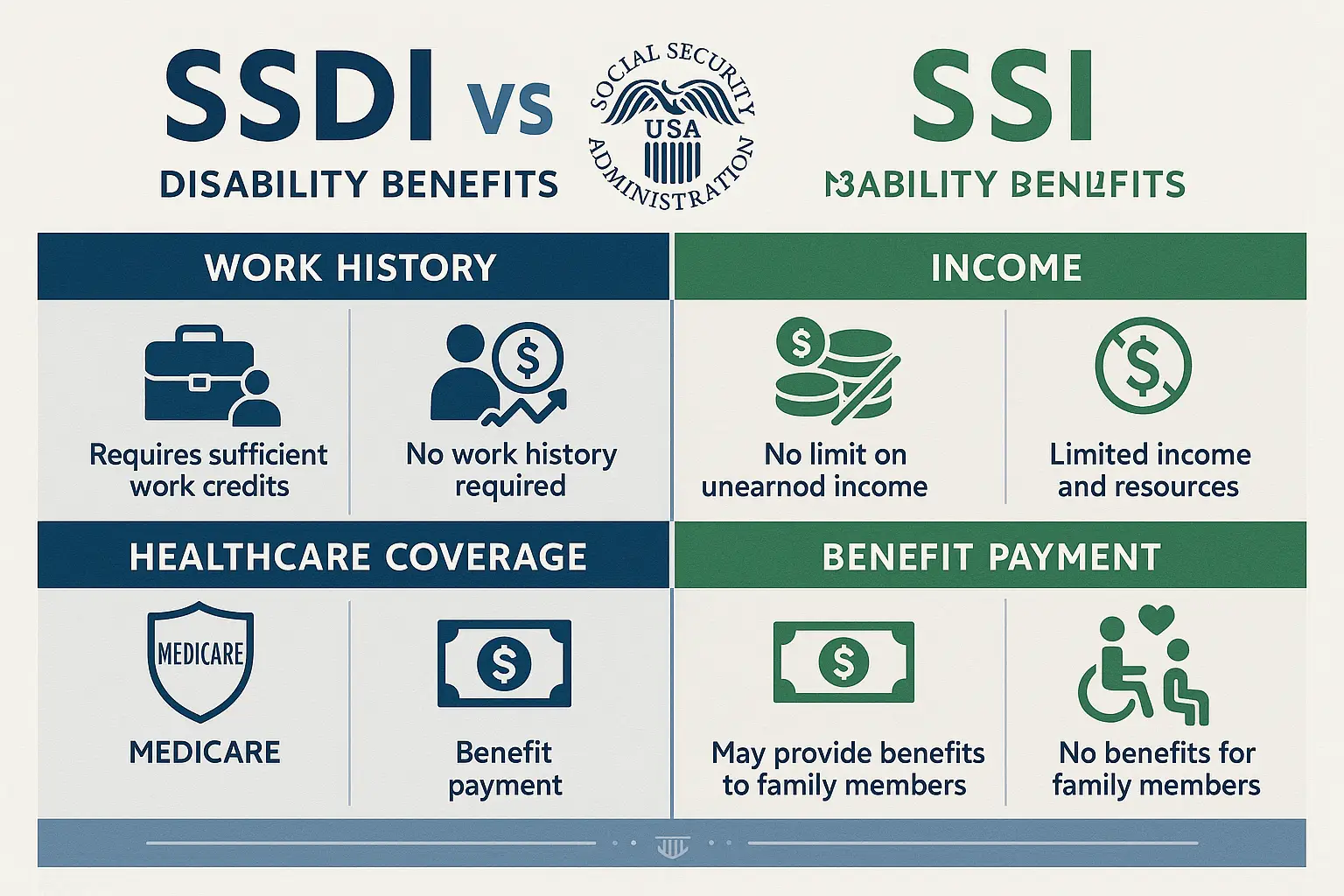

- SSDI is an earned benefit. You must have worked jobs covered by Social Security and paid Social Security taxes. If you later become unable to work due to a severe medical condition, SSDI provides monthly payments.

- SSI is a need-based program. Regardless of work history, it’s designed for people with little or no income or resources.

Understanding which program you qualify for matters because applying incorrectly or waiting too long can delay access to essential disability benefits and health care coverage. In some cases, you may be eligible for both SSDI and SSI simultaneously, a situation called “concurrent benefits.” Knowing your options upfront can save you time and help secure financial stability faster.

What Is SSDI?

Social Security Disability Insurance (SSDI) protects workers who can no longer continue their jobs due to a severe medical condition. It functions like an insurance program: workers pay into Social Security through payroll taxes, and those contributions act as coverage if disability strikes later.

Key Features of SSDI:

- Work Credits Requirement: To qualify, you need enough work credits earned each year you work and pay Social Security taxes. Most workers need around 40 credits, but younger workers may be eligible with fewer. For example, someone in their late 20s may only need a few years of work history.

- Medical Eligibility: Your medical condition must meet the SSA’s definition of disability. This means the impairment prevents you from performing past work and adjusting to a new job and is expected to last at least 12 months or result in death.

- Monthly Benefits: The amount you receive depends on your past wages. In 2024, the maximum monthly SSDI benefit is $3,822, but most people receive less, based on lifetime average earnings.

- Health Care Coverage: After 24 months of SSDI payments, you become eligible for Medicare, which helps cover medical bills, prescriptions, and hospital stays.

- Family Benefits: Certain family members—such as a spouse, minor children, or disabled adult children—may also qualify for benefits under your record. This can provide significant additional support.

Example Scenario:

Imagine a 45-year-old worker who paid Social Security taxes for over 20 years and is suddenly diagnosed with multiple sclerosis. Because they have a strong work history and a severe functional limitation, they may qualify for SSDI. Not only would they receive monthly benefits, but their dependent child could also be eligible, helping the entire household maintain stability.

What Is SSI?

Supplemental Security Income (SSI) works differently. It is not based on work history or Social Security taxes but on financial need. SSI helps individuals with little or no income who are either disabled, blind, or over age 65. The program ensures people with limited resources can still cover basic needs like food, shelter, and clothing.

Key Features of SSI:

- No Work History Required: You don’t need a job background to qualify. Even someone who has never worked a Social Security-covered job may be eligible.

- Income and Resource Limits: Your countable income and assets must fall below set limits to qualify. In 2024, the federal benefit rate is $943 for individuals and $1,415 for couples. Resources like cash, bank accounts, and property (excluding your home) must usually stay below $2,000 for individuals or $3,000 for couples.

- Monthly Benefits: SSI provides a flat monthly payment adjusted for income and living arrangements. It’s generally lower than SSDI but can be life-saving for those without income.

- Health Care Coverage: Most SSI recipients automatically qualify for Medicaid, which covers doctor visits, hospital care, prescriptions, and more.

- Eligible Groups: SSI benefits are available for older adults with limited income, blind individuals, disabled children, and disabled adults who meet strict income and medical requirements.

Example Scenario:

Consider a 67-year-old individual with no work history and very little income. They would not qualify for SSDI because they didn’t pay Social Security taxes. However, they may be eligible for SSI, receiving monthly payments and immediate Medicaid coverage to help with medical expenses.

SSDI vs SSI: Quick Comparison

When comparing Social Security Disability Insurance (SSDI) and Supplemental Security Income (SSI), it helps to see the differences side by side. Many people confuse the two, but each program serves a unique purpose. Understanding these distinctions can help you decide which program may provide the disability benefits you need.