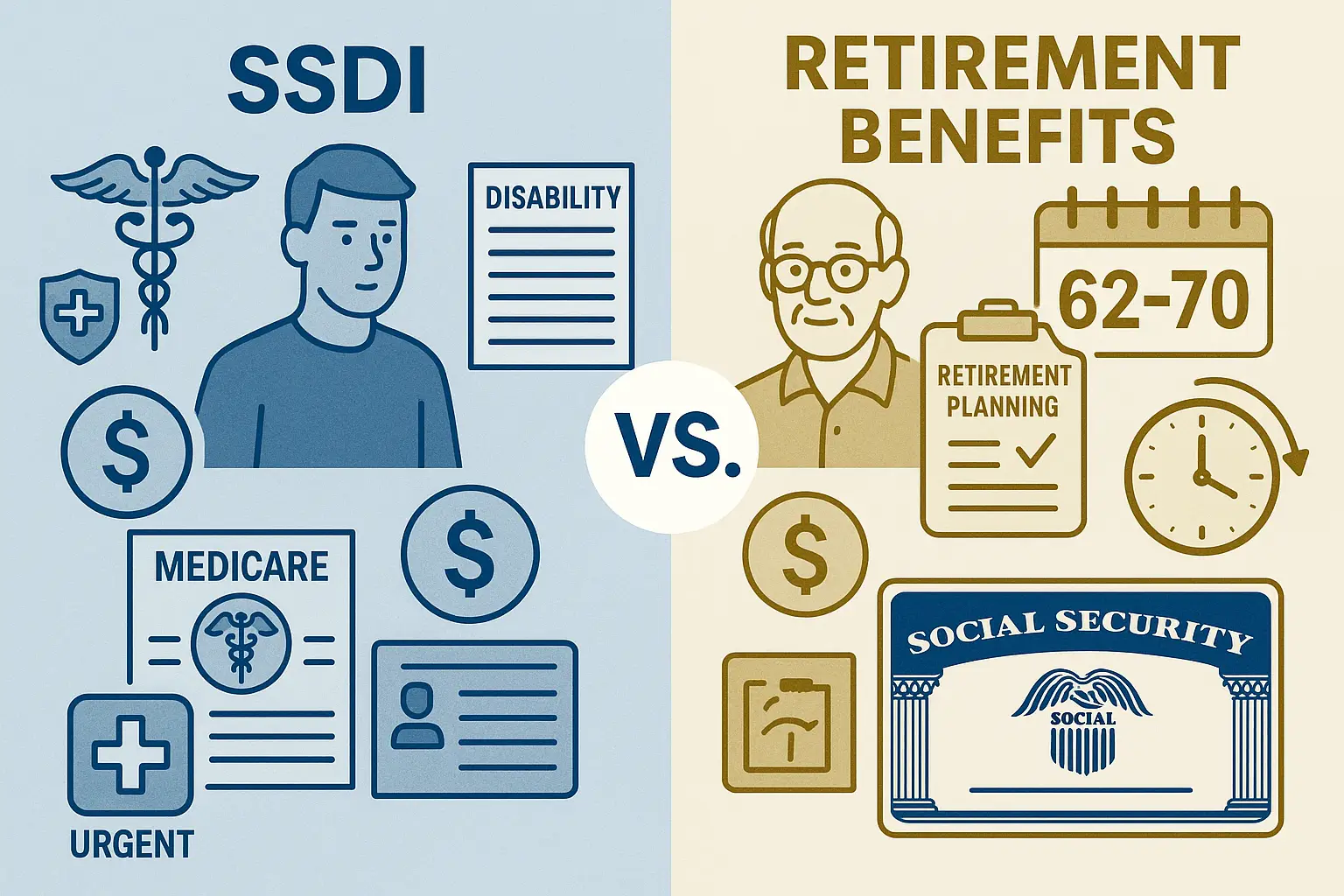

Disability vs Retirement: Why It Matters

The Social Security Administration offers two major programs that provide income support when people can no longer work or choose to retire. Social Security Disability Insurance provides disability benefits to workers who cannot continue employment because of a qualifying medical condition. In contrast, Social Security retirement benefits provide income replacement once a worker reaches retirement age and has earned enough credits by paying Social Security taxes.

These programs share similarities, such as offering a monthly benefit and requiring a work history, but they serve very different purposes. SSDI benefits are based on medical eligibility and proof that a person’s disability significantly limits their ability to work. Retirement benefits, by contrast, are tied to age and work credits, with the option to claim early retirement, wait until full retirement, or delay benefits for a higher payment amount.

Knowing the differences between disability vs. retirement helps workers, former spouses, and dependents make informed decisions about when and how to file. Understanding the rules prevents unnecessary delays, reduces the risk of denied claims, and ensures families can protect their financial future. Whether a person becomes disabled unexpectedly or chooses to retire after years of work, knowing which Social Security program applies is essential for long-term stability.

Social Security Disability Insurance Overview

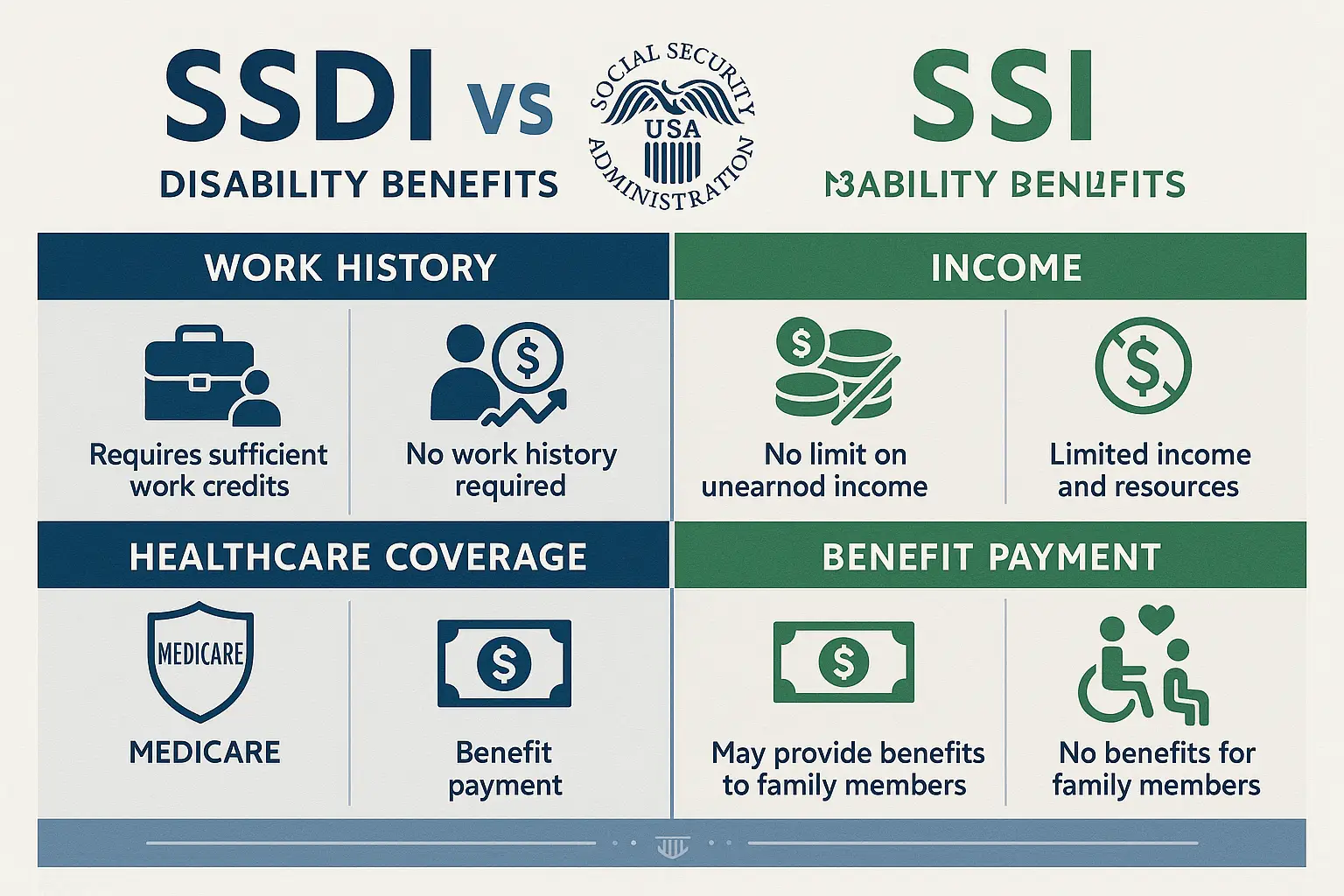

Social Security Disability Insurance is a federal program that pays benefits to disabled workers who have a qualifying work history and a serious medical condition. It is not the same as Supplemental Security Income, which is need-based. SSDI benefits are tied directly to your lifetime earnings and your history of paying Social Security taxes.

Eligibility Requirements for SSDI

Applicants must meet both medical and work credit requirements:

- Medical records must show that the disability prevents you from substantial employment.

- The disability must be expected to last at least one year or result in death.

- Most cases require 40 work credits, with at least 20 earned in the last 10 years.

- Younger workers may qualify with fewer credits depending on their age and disability.

The SSDI Application Process

To file an SSDI application, you must provide documents such as your birth certificate, medical records, and work history. You may apply online, by phone, or at a Social Security office. The process includes a five-month waiting period before you can begin receiving payments.

Benefit Amounts for SSDI

The monthly benefit is based on your average wages and net earnings. The Social Security Administration calculates your Primary Insurance Amount using your lifetime record of covered employment. There is no reduction based on age. After two years, you generally become eligible for Medicare health insurance.

Social Security Retirement Benefits Overview

Social Security retirement benefits provide income to workers who have reached retirement age and earned enough credits through covered employment. These benefits help millions of retirees cover essential costs such as food, housing, and health care coverage.

Eligibility for Retirement Benefits

To qualify, you must:

- Earn at least 40 Social Security credits, typically equal to 10 years of work.

- Reach the minimum retirement age of 62, though benefits are permanently reduced if claimed early.

- To receive your full benefit, you must wait until full retirement age, usually between 66 and 67, depending on your birth year.

- Delay retirement until age 70 to receive increased monthly payments.

The Retirement Benefits Application Process

The Social Security Administration recommends filing a retirement application three months before you want benefits to begin. You can apply online, by phone, or visiting a local Social Security office. Required documents include proof of birth, citizenship, work records, and bank account information for direct deposit.

Benefit Amounts for Retirement

Retirement benefits are also based on average wages and your Primary Insurance Amount. The age at which you decide to retire impacts your monthly benefit:

- Early retirement at 62 pays about 75 percent of your benefit.

- Full retirement pays 100 percent at your full retirement age.

- Delayed retirement until age 70 increases payments to about 132 percent of your benefit.

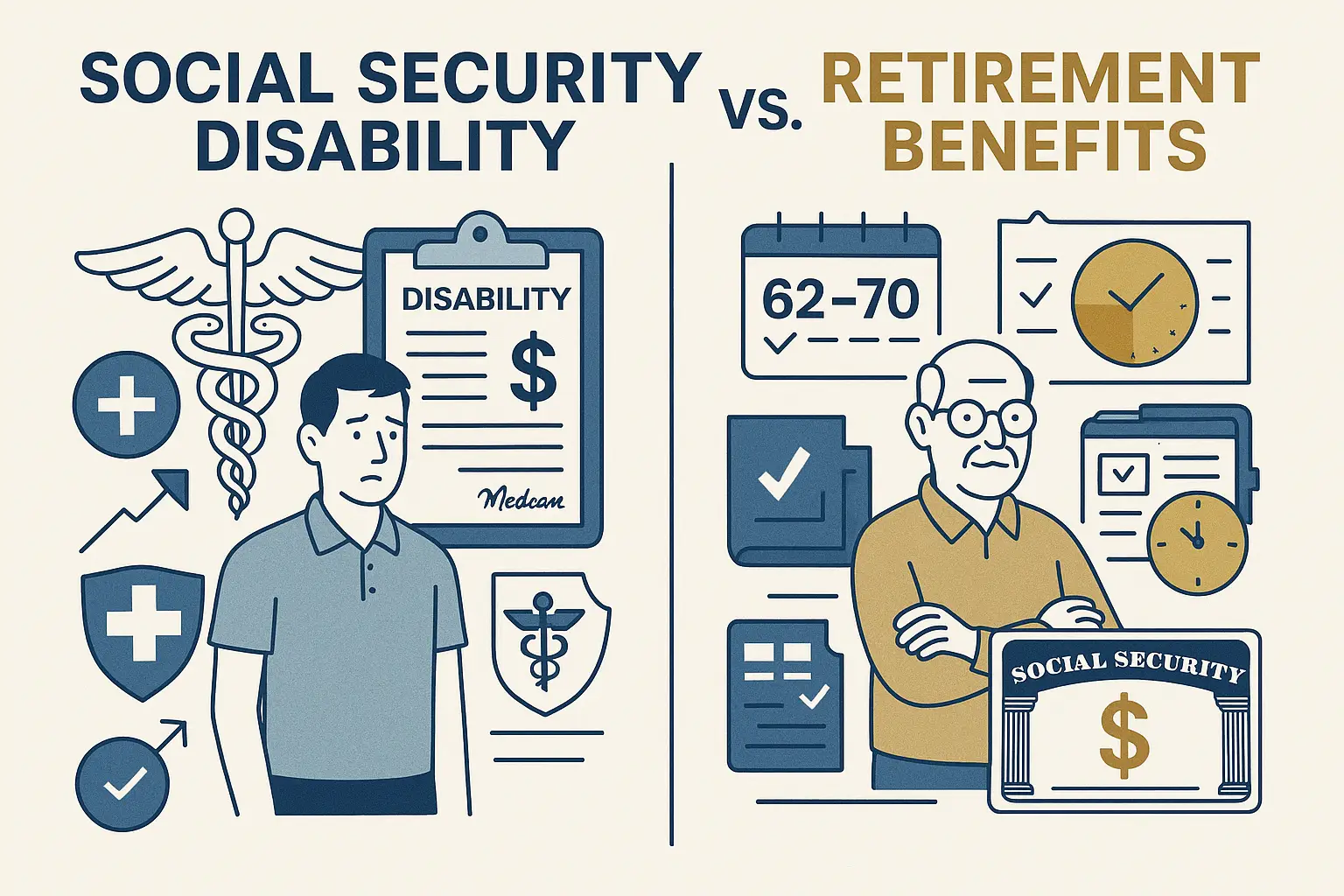

Key Differences Between Disability and Retirement Benefits

Understanding these differences can help workers decide whether to pursue disability benefits, apply for early retirement, or wait until full retirement age.

Timing Considerations: When to File

Deciding when to file for disability vs. retirement benefits depends on age, income, health, and work history.

- File an SSDI application when you become disabled and cannot continue employment. Do not wait for additional documents since you can provide more evidence later.

- File for retirement benefits three months before your desired start date to ensure timely payments.

- Remember that SSDI automatically converts to retirement benefits at full retirement age without any change in benefit amount.

Why Taking Action Quickly Matters

Filing on time with the Social Security Administration is essential to protect your disability benefits or retirement benefits. When workers delay submitting a disability claim or retirement application, they risk losing money that could have been paid as back benefits. In most cases, delays also create gaps in health care coverage and may prevent dependents or a surviving spouse from receiving the full support they are entitled to.

Taking action quickly also ensures you qualify for additional protections, such as Medicare health insurance after two years on Social Security Disability Insurance or automatic enrollment at age 65 for retirement. Timely filing helps you begin receiving your monthly benefit without unnecessary interruptions, reduces the chance of denied claims due to missed deadlines, and gives you faster access to vital programs that cover medical costs, food, and housing.

Awareness of strict timelines is one of the most critical steps in protecting income. For example, SSDI claims include a five-month waiting period, and retirement benefits often require applying three months before you want payments to start. By acting quickly, workers, former spouses, and dependents can avoid unnecessary risk, secure long-term financial stability, and protect their family’s future under Social Security programs.

Our 4-Step Process for Filing Successfully

- Case review – The process begins with a detailed review of your situation, age, work history, and medical evidence to determine whether you may qualify for disability or retirement benefits.

- Eligibility check – At this stage, your information is evaluated against Social Security Act requirements, including disability standards, retirement age, and credits.

- File a claim – Once eligibility is established, all necessary documents, forms, and records are prepared and submitted online, by mail, or at a local Social Security office.

- Ongoing support – After filing, you receive continuous updates, help with appeals if your claim is denied, and clear guidance through each step until payments begin

This structured process ensures you do not navigate complex Social Security programs alone.